Medicaid vs Medicare: Which One Covers You and How to Enroll

Advertising

A Medicaid vs Medicare difference confuses millions of Americans every year.

Cada programa cobre pessoas diferentes — e entender qual se aplica a você pode economizar milhares de dólares.

Keep reading and you will know exactly which one covers you, and how to enroll today.

See Also

- SNAP benefits 2026 — who qualifies and how to apply

- Assurance Wireless free phone — what to know first

- Government phone companies — how to choose the right one

- Lifeline systems — how medical alert systems work

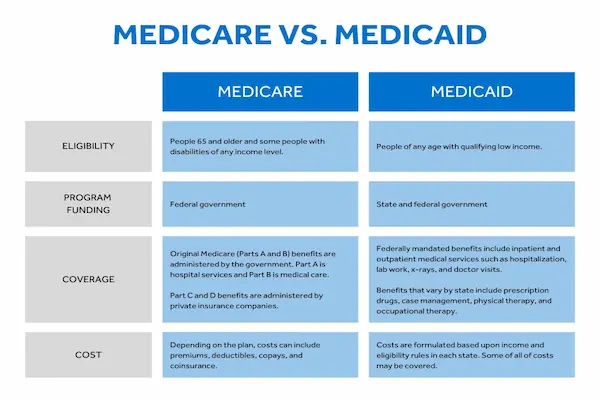

Medicaid vs Medicare Difference: The Core Answer

Medicare is an age- and disability-based insurance program — you earn it through years of work. Medicaid is an income-based assistance program — you qualify based on how much you earn right now.

That single distinction explains why two people living in the same household can be covered by completely different programs, or in some cases, by both simultaneously.

| Feature | Medicare | Medicaid |

|---|---|---|

| Primary Audience | People 65+ or those with specific disabilities | People with low income and limited resources |

| Administration | Federal — same rules in every state | State & Federal — rules vary significantly by state |

| Cost to You | Monthly premiums, deductibles, and 20% coinsurance | Very low or no cost for most covered services |

| Long-Term Care | Generally does not cover nursing home care | Covers long-term nursing home and in-home care |

| Dental & Vision | Not included in Original Medicare | Often included depending on state plan |

Understanding this table is the first step — but the real value comes from knowing exactly what each program covers and what it costs you in 2026.

Medicare Explained: Parts A, B, C, and D in 2026

Medicare is structured in four distinct parts, each covering a different category of care — and each with its own cost in the current year.

Part A — Hospital Insurance

Part A covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health services.

Most people pay nothing for Part A if they or their spouse worked and paid Medicare taxes for at least 10 years. For those who did not meet that threshold, the 2026 premium is up to $518 per month.

The hospital deductible in 2026 is $1,736 per benefit period — not per year, which means multiple hospitalizations in the same year can trigger multiple deductibles.

Part B — Medical Insurance

Part B covers doctor visits, outpatient care, preventive services, and durable medical equipment.

The standard monthly premium in 2026 is $202.90, with an annual deductible of $283. Higher-income enrollees pay more through the Income-Related Monthly Adjustment Amount (IRMAA).

Part D — Prescription Drugs

Part D is one of the most important updates to know for 2026: there is now a $2,100 out-of-pocket cap on covered prescription drugs.

Once you reach that spending threshold in a calendar year, all covered medications drop to $0 for the remainder of the year — a significant change for people managing chronic conditions with expensive prescriptions.

Medicare Advantage — Part C

Medicare Advantage plans are offered by private insurers approved by Medicare and bundle Parts A and B together, often adding dental, vision, and hearing coverage that Original Medicare excludes.

These plans are worth comparing carefully each year during Open Enrollment (October 15 to December 7) because plan networks, premiums, and covered benefits change annually.

Medicaid Explained: Who Qualifies and What It Actually Covers

Medicaid is administered jointly by the federal government and individual states — which means eligibility rules, covered services, and application processes vary depending on where you live.

Income Eligibility in 2026

In states that expanded Medicaid under the Affordable Care Act, adults earning up to 138% of the Federal Poverty Level generally qualify — approximately $1,732 per month for an individual in 2026.

Non-expansion states use narrower eligibility rules, primarily covering low-income children, pregnant women, elderly individuals, and people with disabilities. If you are an adult without children in a non-expansion state, eligibility may be significantly more restricted.

The same low income that qualifies you for Medicaid likely also qualifies you for programs like Assurance Wireless free phone service through the federal Lifeline program — which uses Medicaid enrollment as a direct eligibility trigger.

What Medicaid vs Medicare Coverage Actually Looks Like

Medicaid is consistently more comprehensive than Medicare for low-income enrollees — covering services that Medicare either excludes or only covers partially:

- Dental care: Covered in most state Medicaid plans; not included in Original Medicare.

- Vision care: Eye exams and glasses are typically covered under Medicaid; excluded from standard Medicare.

- Long-term care: Nursing home and in-home care are major Medicaid benefits — this is a critical distinction for families planning for aging parents.

- Transportation to medical appointments: Non-emergency medical transportation is a standard Medicaid benefit in most states.

- No enrollment windows: Unlike Medicare, you can apply for Medicaid at any point during the year — there is no annual open enrollment period.

Medicaid vs Medicare Texas and Other State Differences

For residents asking specifically about Medicaid vs Medicare in Texas, the key fact is that Texas is a non-expansion state — meaning Medicaid eligibility for adults without disabilities or dependent children is significantly more limited than in expansion states.

Texas adults without children generally do not qualify for Medicaid regardless of income, which makes Medicare or Marketplace plans through healthcare.gov the primary coverage path for this group.

In contrast, states like California (Medi-Cal vs Medicare is a common search for residents there) operate under full expansion and offer some of the most comprehensive Medicaid benefits in the country, including full dental, vision, and long-term services.

Dual Eligibility: When You Qualify for Both Medicare and Medicaid

If you are 65 or older with low income, you may qualify as dual eligible — enrolled in both programs simultaneously — which is one of the most financially beneficial positions in the US healthcare system.

Here is exactly how dual coverage works in practice:

- Medicare pays first for hospital stays, doctor visits, and outpatient care.

- Medicaid pays second, often covering the Medicare premiums, deductibles, and the 20% coinsurance that Medicare leaves unpaid — effectively reducing your out-of-pocket cost to near zero.

- Extra Help on Part D: Dual-eligible individuals automatically receive the federal “Extra Help” subsidy for prescription drug costs, which dramatically reduces monthly medication expenses.

Dual-eligible individuals who also qualify for Lifeline medical alert systems and phone programs can layer additional federal benefits on top of their healthcare coverage — since Medicaid enrollment is a qualifying trigger for several non-healthcare assistance programs as well.

2026 Medicaid Work Requirements: What Changed This Year

Some states are introducing new Medicaid work requirements for adults aged 19 to 64 in 2026 — a development that affects non-disabled, non-elderly enrollees in participating states.

If your state has implemented these rules, you may need to document at least 20 hours per week of employment, job training, or qualifying community service activity to maintain your coverage.

This mirrors the SNAP work requirement changes from the same fiscal year — and the two programs share eligibility in ways that mean changes to one can affect your standing in the other. You can review the full SNAP rules in our guide to SNAP benefits eligibility 2026.

Is Medicare and Medicaid the Same Thing?

No — and this is the single most common misconception about both programs.

Medicare is an earned insurance benefit tied to age or disability status, funded primarily through payroll taxes during your working years.

Medicaid is a means-tested assistance program funded jointly by states and the federal government, with eligibility determined by current income and resources — not work history.

While both programs can cover the same person simultaneously if they qualify under each set of rules, they operate through completely separate systems, separate application processes, and separate coverage structures.

This content is purely informational. We have no affiliation with, sponsorship from, or control over any government program, insurance plan, or third-party platform mentioned here. Eligibility rules vary by state and change frequently. Always verify your specific situation directly with Medicare.gov, your state Medicaid office, or a licensed benefits counselor before making any enrollment decision.

Ready to explore every federal benefit available to your household? Our Public Assistance section covers healthcare programs, food assistance, phone subsidies, and every major benefit worth knowing about in 2026.